It’s good to be back from vacation and refreshed after following the weak market over the month of May. As I was away, The New York Times was delivered to my door each morning (complimentary) and I found an interesting article. I have always been amazed by the enormous incomes that hedge fund managers produce year in and year out. I have even posted up the top 10 salaries from past years (example:

Top Incomes in 2003 for Hedge Fund Managers ). If you briefly view the top 10 from 2003, you can see that George Soros was #1 with a take home pay of $750 million. Well, only two years later the top earner has doubled the total from 2003 to a whopping $1.5 billion (eclipsing last year’s top earner by $500 million). Edward Lampert was the first manager to surpass the billion dollar mark in 2004 but two men accomplished the feat last year. One of my favorite traders, Steven A. Cohen remained in the top 10 with a salary of $550 million. Mr. Cohen, along with several others on the list below has been featured in the book series titled: Market Wizards (all highly recommended). Below is the entire article from

The New York Times written by Jenny Anderson (originally printed on May 26, 2006):

Enjoy, the numbers are staggering!

Atop Hedge Funds, Richest of the Rich Get Even More So

By JENNY ANDERSONPublished: May 26, 2006

*image from The New York Times website*

Talk about minting money. In 2001 and 2002, hedge fund managers had to make $30 million to gain entry to a survey of the best paid in hedge funds that is closely followed by people in the business. In 2004, the threshold had soared to $100 million.

Last year, managers had to take home — yes, take home — $130 million to make it into the ranks of the top 25. And there was a tie for 25th place, so there were actually 26 hedge fund managers who made $130 million or more.

Just when it seems as if things cannot get any better for the titans of investing, they get better — a lot better.

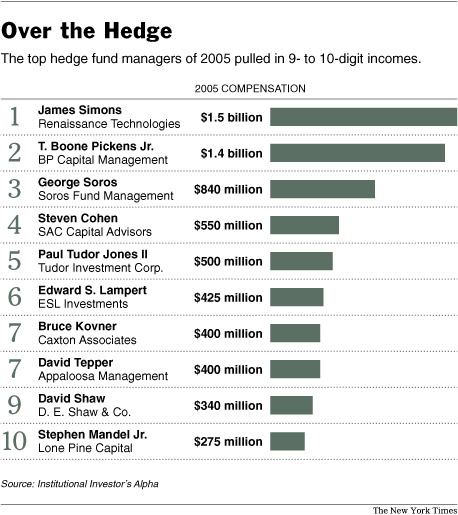

James Simons, a math whiz who founded Renaissance Technologies, made $1.5 billion in 2005, according to the survey by Alpha, a magazine published by Institutional Investor. That trumps the more than $1 billion that Edward S. Lampert, known for last year's acquisition of Sears, Roebuck, took home in 2004. (Don't fret for Mr. Lampert; he earned $425 million in 2005.) Mr. Simons's $5.3 billion flagship Medallion fund returned 29.5 percent, net of fees.

No. 2 on Alpha's list is T. Boone Pickens Jr., 78, the oilman who gained attention in the 1980's going after Gulf Oil, among other companies. He earned $1.4 billion in 2005, largely from startling returns on his two energy-focused hedge funds: 650 percent on the BP Capital Commodity Fund and 89 percent on the BP Capital Energy Equity Fund.

A representative for Mr. Simons declined to comment. Calls to Mr. Pickens's company were not returned.

The magic behind the money is the compensation structure of a hedge fund. Hedge funds, lightly regulated private investment pools for institutions and wealthy individuals, typically charge investors 2 percent of the money under management and a performance fee that generally starts at 20 percent of gains.

The stars often make a lot more than this "2 and 20" compensation setup. According to Alpha's list, Mr. Simons charges a 5 percent management fee and takes 44 percent of gains; Steven A. Cohen, of SAC Capital Advisors, charges a management fee of 1 to 3 percent and 44 percent of gains; and Paul Tudor Jones II, whose Tudor Investment Corporation has never had a down year since its founding in 1980, charges 4 percent of assets under management and a 23 percent fee.

They may charge such amounts because they can. "In the end, what people want is the risk-adjusted performance," said Gordon C. Haave, director of the investing and consulting group at Asset Services Company, a $4 billion institutional advisory business. "As long as the performance is up there, in the end the investors do not care about the high fees."

If there is a downside to being so rich, it is that the money is flooding in at a time when hedge fund performance, even for some of the greats, has been less than stellar over all. Six managers made the top 25 even while posting returns in the single digits.

"You would think someone would be a little embarrassed taking all that money for humdrum returns," said John C. Bogle, founder of the Vanguard Group. "I guess people don't get embarrassed when it comes to money."

Many of the funds have gotten so big that the management fees alone are the source of much wealth, perhaps leaving some managers without the fire to try to outdo the broad market. Institutions like pension funds and endowments, whose money is fueling a significant part of the hedge fund boom, continue to flock to these managers for their track records and name recognition.

Bruce Kovner's Caxton Global Offshore fund returned 8 percent last year while his Gamut Investments, an offshore fund he runs for GAM Fund Management, returned 6.4 percent. The survey said 2005 was the third year that he had posted single-digit returns. Still, Mr. Kovner took home $400 million, according to the list. He did not return calls to his office.

The average take-home pay for the 26 managers in 2005 was $363 million, a 45 percent increase over the top 25 the previous year. Median earnings surged by a third, to $205 million last year, from $153 million in 2004.

Included on the list were both familiar names and new stars. Mr. Cohen of SAC Capital, who while shunning publicity has become known as an avid art collector, landed in fourth place in 2005, taking home $550 million. For the year, his various funds were up 18 percent on average. A spokesman for Mr. Cohen declined to comment.

New to the list are two managers from Atticus Capital, a fund that was among the investor activists that opposed Deutsche Börse's attempted takeover of the London Stock Exchange for $2.5 billion. That campaign led to the ouster last year of the Deutsche Börse chief executive. Atticus is also a major participant in the battle for Euronext, the pan-European stock and derivatives exchange, which is being courted by the New York Stock Exchange and by Deutsche Börse.

Making his debut at 14th place, Timothy Barakett made $200 million in 2005. His Atticus Global Fund was up 22 percent net of fees, while the European Fund, managed by 33-year old David Slager (No. 20 on the list with $150 million), soared 62 percent. Atticus officials did not respond to requests for comment.

A fellow investor activist, Daniel Loeb of Third Point, made $150 million in 2005. According to Alpha, only 10 percent of the firm's $3.8 billion is dedicated to activism, an unexpectedly small slice considering his reputation as management's worst nightmare.

A value- and event-driven manager, Mr. Loeb posted returns of 18 percent, largely from bets in energy, including a 140 percent gain on McDermott International. Mr. Loeb's spokesman declined to comment.

Another debut on the list was by William F. Browder, founder and chief of Hermitage Capital Management and the largest foreign investor in the Russian stock market. He tied for 25th place by taking home $130 million.

Mr. Browder, 42, grandson of Earl Browder, onetime leader of the Communist Party of the United States, has been barred from returning to post-Communist Russia since November, when immigration officials revoked his visa. The fund had $4.3 billion under management and in 2005, his flagship Hermitage Fund was up 81.5 percent.

A shareholder activist, he has challenged management at Russian state giants including Gazprom and Lukoil. Mr. Browder could not be reached for comment.